As you know, the ultimate goal of any business is to make money. No matter what business you start, no matter what resources you use, no matter what processes you employ to generate profit, in the end only one thing matters: whether the company is profitable, how profitable it is, and the actual financial result is often the basis for the company's further development strategy.

To calculate how much profit a company has made, you need to subtract the company's expenses from its revenues. At first glance, this is a simple and straightforward formula. But is it really that simple? While the income is more or less clear, when it comes to calculating the expenses, it is important what kind of calculation method is used in the accounting.

In this regard, companies involved in trade and manufacturing deserve special attention. In such companies, one of the largest cost items is the cost of goods sold.

What Is the cost of Goods Sold in Terms of IAS 2 Inventory?

Cost of Goods Sold (COGS) is the direct cost of the manufactured goods that a company has sold. These costs consist of the price of materials and the wages of workers directly involved in the production process. It does not include indirect costs such as distribution costs and sales agent fees.

Materials or goods that can be stored in a warehouse are referred to as inventory.

According to IAS 2, there are several methods of measuring inventory. The following are the most commonly used methods:

- Specific identification method;

- Weighted average cost method;

- FIFO method.

Each of these methods has its own peculiarities of application, and depending on which inventory valuation method we choose, the resulting cost of goods sold may differ. And that, in turn, has a direct impact on the company's profit margin.

In addition, every company needs a useful and reliable system for determining both the quantity and value of inventory. In fact, these are the key indicators for accounting in a company with inventories. And here it is important to understand that there are different approaches to the organization of such calculations: records of stock movements in the warehouse can be made continuously, i.e. at the end of each transaction, or at certain intervals, if they do not cause significant distortion of the data. In practice, two main systems of quantitative inventory accounting are used: the periodic system and the continuous system.

In this article, we will look at how the FIFO method is used in the periodic system.

Periodic Inventory System

The very name of this accounting system indicates the presence of a certain periodicity in the approach. The period here is one calendar month. With periodic inventory accounting, the actual inventory balance is determined at the end of each calendar month; during the period there is no operational accounting of inventory movements or balances, and the opening balance at the beginning of the period is the inventory balance determined by the inventory count at the end of the previous period. In this way, we have only two periodic entries: one at the beginning of the month and one at the end of the month.

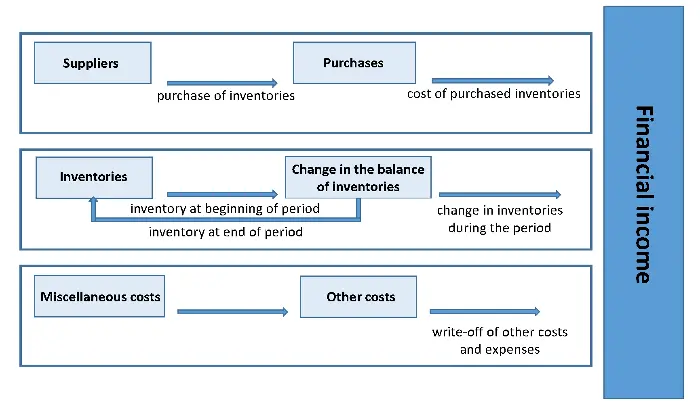

If we summarize what has been said above and present it in the form of a diagram, then the scheme of inventory accounting according to the periodic system will look as follows:

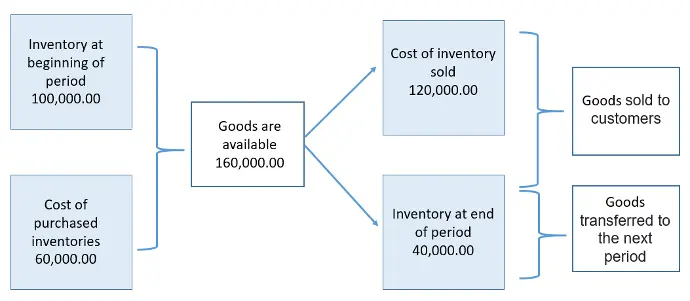

In order to have a better understanding of how the cost of goods sold is calculated, the calculation scheme can be presented in the following way:

According to this approach, the difference between the cost of the inventory available for sale and the cost of the actual inventory at the end of the month must be deducted to arrive at the cost of goods sold at the end of the period. At the end of the period, an entry is recorded that clears the beginning balance, which is the balance at the end of the previous period, and adds the ending balance, which is the balance at the end of the current period. In other words, these are essentially the only entries made to the inventory account for the entire period.

Since the inventory is taken once a month, we have the fact that in real-time accounting the amount of stock available in the warehouse is only relevant on the balance sheet date. As soon as a transaction (purchase or sale) takes place, this amount becomes irrelevant in real time and remains the indicator of the previous period until a new inventory amount is entered at the end of the next accounting period.

Thus, it is clear that the periodic inventory system is not transparent enough, since it does not provide an accurate value at any specific date during the period, except for the date of the inventory itself. Nevertheless, this inventory system is quite common among small enterprises with relatively small sales volume because it does not require much work. But with the spread of computer development, there is a tendency for its gradual loss of popularity. For large enterprises, such an accounting system is not effective enough, because the lack of accurate real-time data with large turnover volume can lead to loss of sales or high operating costs.

FIFO (First-In-First-Out)

The first-in, first-out (FIFO) method assumes that those items of inventory that were purchased or produced first are sold first. Accordingly, the items remaining in inventory at the end of the period were purchased or produced last.

The FIFO method is typically used for storage of products that have a very limited shelf life, but not only for these products.

This method assumes that goods are used/sold in the order in which they are purchased and that the remainder of the inventory is the last purchase.

FIFO Method - Periodic Accounting

If a company uses a periodic accounting system and valuates its inventory using the FIFO method, how does this work in real data?

To illustrate, let's look at the following example.

Let's say that during a period we purchase the same item on different dates at different purchase prices and sell a certain amount of the item:

Date

Purchase

Sale

Balance

1 November

2000 units at 40.00 CAD

2000

15 November

6000 units at 44.00 CAD

8000

19 November

4000 units at 60.00 CAD

4000

30 November

2000 units at 47.50 CAD

4000 units at 60.00 CAD

6000

There is no difficulty in calculating the quantity. But how do we calculate the cost of goods sold?

First, let's calculate the cost of purchased goods, which is easy to do:

Date

Purchase

Unit Cost

Cost

1 November

2000 units

40.00 CAD

80000,00 CAD

15 November

6000 units

44.00 CAD

264000,00 CAD

30 November

2000 units

47.50 CAD

95000,00 CAD

Total

439000,00 CAD

At this point, we need to calculate the cost of the inventory at the end of the period.

Since the FIFO method assumes that the inventory purchased first will be sold first and the inventory remaining at the end of the period will be purchased last, the cost of inventory at the end of the period is as follows:

Date

Date

Date

Purchase

Unit Cost

Cost

Date

Date

15 November

4000 units

44.00 CAD

176,000.00 CAD

Date

Date

30 November

2000 units

47.50 CAD

95,000.00 CAD

Date

Date

Total

271,000.00 CAD

As a result of our calculations, we find that cost of sales is equal to: 439000-271000 = UAH 168000.00

Periodic Inventory Accounting System in ERP Odoo

What settings do you need to make to properly configure periodic accounting when using the Odoo system?

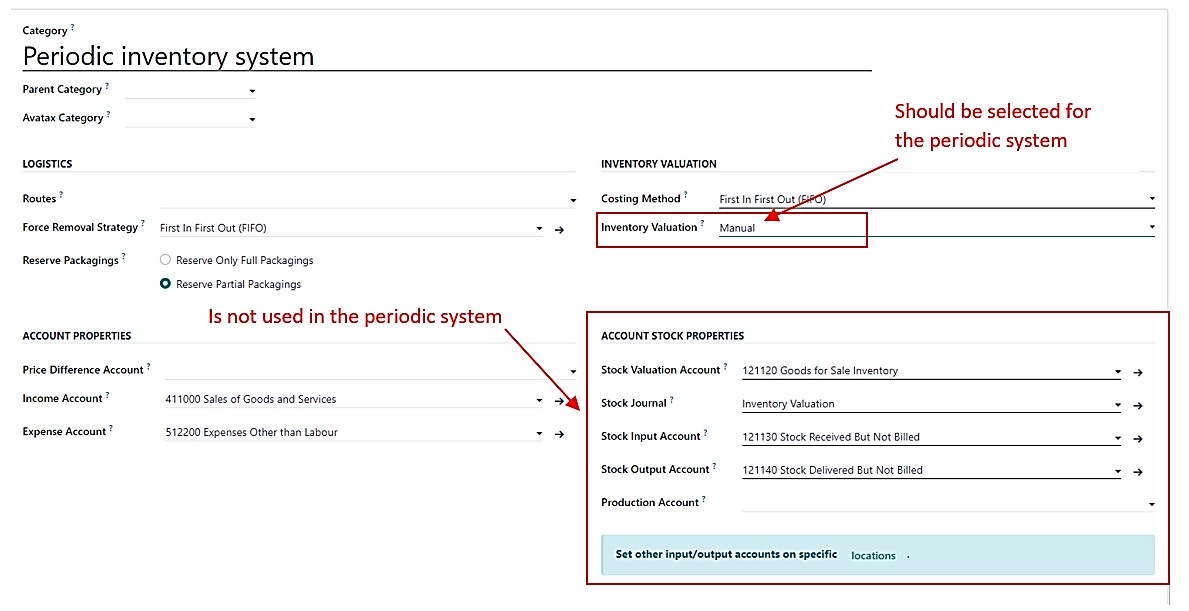

First of all, you have to keep in mind that Odoo supports two inventory accounting systems: periodic and continuous. Accounting settings are defined at the product category level:

If you are an Odoo user and use the periodic inventory system and the FIFO method in your company, then you need to know what the correct settings are in the system to account for inventory correctly.

First of all, it is necessary to keep in mind that Odoo supports two systems of inventory accounting: the periodic one and the perpetual one. In Odoo, many of the settings that determine or affect the movement of inventory are set at the level of the products we deal with or their categories. And it is the inventory accounting settings that are defined at the product category level. For those product categories that use FIFO, the Costing Method field should be set to FIFO, and Inventory Valuation should be set to Manual. When these settings are made, the Accounting Stock Properties group of settings becomes irrelevant and is not displayed in your Product Category card, as shown in the screenshot below:

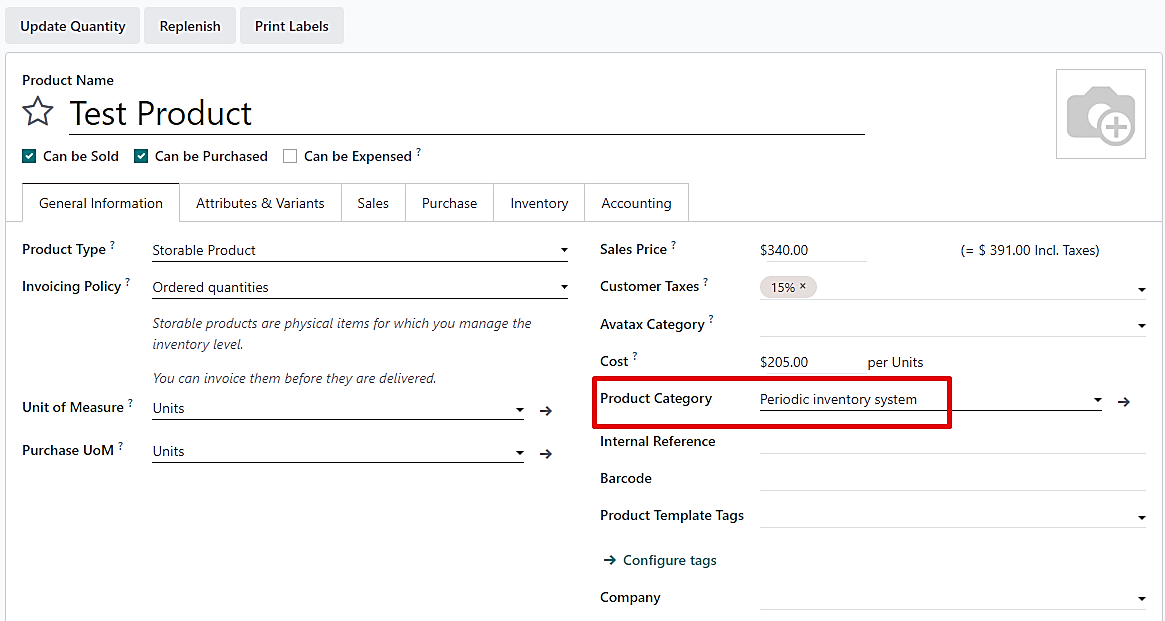

So, after we set up the appropriate category, we move on to the products themselves. Each product that is entered into the system has to belong to a certain category. This is indicated in its card on the General tab in the Product Category field. This can be seen in the screen shot below:

With these settings, the system does not expect accounting entries to be made as goods move through the warehouse, as was the case with continuous accounting, where Inventory Valuation should be set to Automatic. However, you shouldn't worry about not having current balances online. In ODoo, you can always see the balances on any date and the value of those balances using the warehouse reports. With the right accounting setup, you can also see the purchases made from suppliers for a certain period. At the end of the period, you will need to make manual journal entries to record the value of the inventory sold.