In the retail industry, inventory is a critical asset - whether you are selling groceries, furniture, or cars. And the performance of that asset depends on how well it is managed and how well it is controlled. With the right approach to inventory, the business will remain profitable. Sales will be maximized, and excess merchandise and write-offs will be kept to a minimum. So what is inventory control?

In fact, both inventory management and inventory control help maintain the financial stability of the business and meet customer demand. For this reason, inventory control and inventory management are often used interchangeably.

It is a complex chain of processes that controls

the storage, replenishment, classification, warehousing, distribution, and

tracking of products. Inventory management is a complex and multifaceted

process. Let's start with a definition of the main functions and elements that

are involved in inventory control activities.

Elements and Functions of Inventory Control

If we take a comprehensive look at the inventory control system, we can identify the following key functional aspects

- Specification and categorization of goods, their identification numbers and types;

- Storing serial number and lot information;

- Implementation and control of barcodes;

- Prioritization of goods using ABC analysis;

- Replenishment process, methods and routes;

- Internal warehouse logistics;

- Inventory list management;

- Real-time warehouse reports;

- Tracking the location of goods in real time;

- Inventory control;

- Accounting and tax operations related to warehouse management;

- Synchronization of stock levels with sales.

Why do You Need to Know How to Control Inventory?

Failure to control inventory can lead to delays in order fulfillment or excess inventory. Excess inventory threatens financial performance and customer loyalty. Excess inventory is a collection of unsold goods that freezes working capital and eventually becomes illiquid inventory that must be written off or liquidated. In addition, storing excess inventory requires additional costs on the part of the company, increases their cost price and negatively affects the bottom line. On the other hand, a shortage of inventory leads to reduced sales, which means lost profits and customer dissatisfaction because the seller cannot deliver the goods they want on time. When inventory control is implemented correctly, a company has complete control over its inventory management.

Optimizing inventory control processes helps a company streamline supply chain processes and reduce logistics, warehousing, and transportation costs.

Inventory Control Methods

Thus, we have established that helping retailers to

efficiently spend money on replenishment and increase cash flow through

rational internal control over the warehouse are the main functions of

inventory management systems. Next, let's take a look at the main methods of

inventory control, which are the most common and suitable for different

companies, depending on their type of activity and business specifics.

Just-in-Time Management (JIT)

Just-in-time (JIT) is a supply chain policy introduced by Toyota in the 1960s that requires materials, goods, and services to be delivered exactly when they are needed for a job or process. The primary goal of the approach is to reduce inventory, waiting time, and spoilage. "

"Just-in-time is a fairly common logistics concept. The basic idea of the concept is this: if a production schedule is established, it is possible to organize the movement of material flows in such a way that all materials, components, and semi-finished products arrive in the required quantity, at the right place, and at the right time for the production, assembly, or sale of finished products. This eliminates the need for safety stock, which can freeze up the cash flow of a company. The just-in-time approach is also one of the basic principles of lean manufacturing.

At the same time, inventory management under JIT can be risky. If demand increases unexpectedly, the manufacturer may not be able to obtain the inventory needed to meet that demand. Even the slightest delay can become a problem and lead to a shortage of goods or a halt in production. The result can be damage to the company's reputation with customers and loss of business to competitors.

Materials Requirement Planning (MRP)

The MRP methodology is the planning of material and resource requirements based on a production/sales plan that is based on production volumes and involves the creation of requests to replenish the company's necessary inventory.

The MRP methodology was first developed in the United States in 1950. However, it did not become widespread and popular until the development of high-speed computer technology in the 1970s. Most companies in the U.S. and U.K. were using or planning to use systems based on the MRP methodology by the end of the 1980s.

The main tasks that the MRP methodology aims to solve are as follows

- Calculate the company's inventory requirements;

- Identifying and maintaining the minimum possible stock levels in the warehouses when calculating requirements;

- Linking the timing of order processing, production operations, inventory delivery and procurement operations.

In other words, the MRP methodology allows you to understand when and in what quantities specific units should be produced based on the overall sales plan. You can then calculate the quantities and timing of the purchase and release of the necessary inventory. Ultimately, a manufacturer will not be able to fill orders if it cannot accurately forecast sales volumes and plan inventory purchases to match those volumes.

Economic Order Quantity (EOQ)

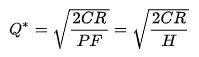

This control method is based on the concept of Economic Order Quantity (EOQ). The concept of Economic Order Quantity (EOQ) is a model that determines the optimal order size of an item that minimizes the total variable costs associated with ordering and inventory holding.

EOQ is determined by a formula developed by Ford W. Harris in 1913 and improved over time.

EOQ

is calculated based on total cost. Total cost can be represented as a

function:

Q* - Efficient Order Quantity (EOQ)

C is the cost of placing an order (does not depend on order size)

R - monthly demand of the product

P is the cost of purchasing one unit of product

F - inventory carrying cost ratio; the portion of the purchase cost of the product that is spent on inventory costs (usually 10-15%, although under certain circumstances it can be set between 0 and 1)

H - inventory cost per unit per month (H = PF)

However, it should be noted that the application of this method is based on certain assumptions:

- Demand for the product is known.

- The time of order fulfillment (delivery) is known and constant.

- Receipt of goods is immediate.

- Wholesale discounts are not considered in the model.

- Shortages are not allowed

This fact makes it difficult or impossible for the formula to account for events such as changes in customer demand, seasonal changes in inventory costs, lost sales due to out-of-stocks, or purchase discounts that a company may take to purchase more inventory

Days Sales of Inventory (DSI) Method

The use of a metric called Days Sales of Inventory (DSI) is another fairly common control method used by companies to track their inventory and monitor their sales. Days Sales of Inventory is a financial metric that shows the average time, in days, it takes a company to convert inventory into sales. The calculation of this ratio also takes into account work in progress. DSI is also known as the average age of inventory. In order to calculate this ratio, the inventory (including work in progress) must be divided by the cost of sales and then multiplied by the number of days in a year (quarter or month). The formula for calculating DSI is as follows

DSI = (Ending Inventory / Cost of Goods Sold) x 365

On the other hand, it should be noted that the DSI is an indicator that analysts use in the determination of sales performance. This is because the DSI also indicates how efficiently a company manages its inventory. What can a high DSI indicate? A high DSI may indicate that the company is not managing its inventory effectively or that it is holding inventory that is difficult to sell.

However, this figure should be treated with caution, as it often lacks context. DSI tends to vary widely across industries and depends on many factors, such as product type and business model. Comparisons between similar companies in the same industry are therefore important. For example, companies in the technology, automotive, and furniture industries can afford to carry inventory for long periods of time. Companies selling perishable or fast-moving consumer goods (FMCG) cannot. Therefore, industry comparisons should be the basis for calculating the DSI index.

ABC Analysis

For any business that has inventory, it is important to have an understanding of the timing and quantity of material orders. With a large nomenclature, it is not possible to analyze every item in the nomenclature. To simplify this problem, an ABC analysis is performed.

The method is based on the well-known "Pareto rule" mentioned above: 20% of the effort produces 80% of the result and vice versa.

It distinguishes between three categories of inventory, called A, B, and C. Category A includes the most expensive goods, which means that a small amount of inventory is held. Category B includes medium-value inventory with a medium frequency of sales. And Category C inventory has the lowest cost but the highest sales frequency and requires less inventory control than Categories A and B.

The purpose of this analysis is to provide a simple and clear ranking of resources, which will allow you to set priorities, identify bottlenecks, and take corrective actions in a timely manner.

Which criterion to use to select these 80% - profit or sales - depends on the purpose of the analysis. If profit is the basis, we rank inventories by marginal revenue. If sales, then by turnover (volume of products sold).

In Summary

Inventory control is a process that allows

companies to track and effectively manage their inventory in order to maximize

profits. There are several inventory control methods. Each method has its

advantages and disadvantages depending on the size and characteristics of the

inventory. The decision on which of the control methods to choose is solely up

to each company. The purpose of this article is simply to delve deeper into the

topic and help you better understand the different inventory control methods so

that you can improve your inventory management processes and your financial

performance by choosing the one that best suits your needs.